Nick Radge: The Chartist (A Systematic Trading Expert)

Table of Contents

Who Is Nick Radge?

Recently I’ve been fascinated by the work of Nick Radge – aka TheChartist.

Nick is a veteran Australian stock trader who began his apprenticeship in the craft of navigating financial markets way back in 1985, during the days of the pits.

He is also the author of the excellent trading book Unholy Grails which is full of gems of practical trading wisdom and techniques:

Nick began his career as a young man straight out of high-school when a family friend offered him a low-level clerical job in a blue chip Australian stock broking firm.

While walking through the private client area of the firm’s office one day, something interesting caught his eye.

He noticed a man drawing red and blue lines on some chart paper. Nick’s life took an interesting turn when he asked the man what he was doing, and discovered that he was manually plotting a five and ten day moving average crossover strategy on a futures market.

This intrigued Nick, and set him down the path of becoming a student of the craft of trend-following and technical analysis based trading systems.

When Nick left work that day he stopped by the stationary shop and bought some chart paper, a red pen, a blue pen, and a black pen – and began plotting his future.

Note: Nick Radge runs a signal service through his company TheChartist where you can follow the exact trades he takes with several of his trading systems. I personally use this service to manage a portion of my capital – if this sounds interesting to you click here to get 10% off your annual subscription (includes 2-week free trial).

Nick’s Trading Style & Philosophy

These days Nick is a professional trader, analyst, consultant, educator and author.

During his early career he was a trader on the floor of the Sydney Futures Exchange, and he also worked for international banks in London, Singapore & Sydney. Over the course of his career he became an expert in systematic trading strategy design and technical analysis.

Nick’s philosophy in both trading and investing is simple. By employing a handful of effective market filters, you can ensure that the strongest stocks in the market will bubble to the top of your watchlist.

And then, to paraphrase his own words – all he needs to do is stick his thumb out and hitch-hike a ride.

Nick often compares trend-following to hitch-hiking. He likens his approach to trading to a hitch-hiker’s approach to getting a ride.

First they decide where they want to go, then they put themselves on the right side of the highway with their thumb out, and then if they’re lucky someone picks them up and not only doesn’t murder them, but takes them all the way or at least close to where they want to go. Nick essentially emulates this approach in his trading.

He doesn’t know which car is going to pick him up, or how far it will take him towards his destination – but if he puts himself in the right place at the right time and looks for the right clues and signs, he’ll eventually find a ride that will take him towards profit town.

He also believes it’s unnecessary to spend too much time (or any time for that matter) investigating a stock’s fundamentals, which is a belief I also share. This is because price action doesn’t lie. Either a stock is strong, or it is not strong.

And if it is strong, then it will tell you on the charts – in the form of breakouts and bullish momentum.

All you need to do is hop on when a stock or asset shows strength relative to the overall market. Obviously it is not so simple as just buying something that is going up – there is more nuance to trend-following than that, which we’ll talk about later.

Now, buying UNDER-VALUED stocks is a different story (and a different strategy).

Nick is essentially a purist trend-follower, like the famously successful trend-followers before him. For instance, he was heavily inspired by the notorious Turtle Traders (and even worked alongside them for a time) in his early days as a trader, and some of his trading systems have been directly inspired by the original Turtle strategies.

Trend-followers like the classic Turtle traders don’t buy under-valued stocks. That goes against their entire philosophy. They buy STRENGTH, not weakness. They buy breakouts. Sometimes they might buy pullbacks, but this is not the same as buying stocks or markets that are weak.

That’s not to say that buying weak markets or “mean-reversion” strategies don’t work. In fact, Nick Radge also employs some mean-reversion and short-term strategies in his own portfolio. There is definitely an edge in buying weakness – IF you employ the methods properly and consistently.

The point I’m trying to make here is not that trend-following is better than mean-reversion or whatever, but rather that there are many, many ways to extract profits out of the markets – you just need to find what works for YOU, and it needs to be something you have the confidence to stick to even when times get bad.

And times WILL get bad at some point.

There is no escaping the Inevitable Drawdown.

Drawdowns

There is no such thing as a strategy that is immune to drawdown.

You can limit your drawdown by employing various risk management techniques or portfolio diversification (both in the markets you trade and the strategies you trade) – but you will not escape the Grim Reaper of the markets.

You cannot avoid drawdowns, just as you can’t avoid tax (unless you’re a multi-national corporation or you have enough capital to set up shop in Belize).

As Nick says:

Drawdowns are the ‘cost’ of exploiting a risk premium and cannot be avoided. However, the ability to stay with a strategy during a drawdown is one of the most difficult aspects all traders face.

Nick Radge – 4 Ways To Trade Through Drawdowns

Most traders struggle to stick to a system during a losing streak or a period of profit stagnation.

The less experienced a trader is, the more likely it is they will suffer from this anxiety and trepidation, and in turn sabotage themselves by ignoring signals, breaking their risk model rules, system hopping or otherwise behaving inconsistently and irrationally.

The more confidence you have in your strategy or system, the more likely you will be to stick with it during tough times – and one strategy or trading style that has stood the test of time over the past several centuries is trend-following.

One of the most attractive aspects of trend-following strategies is that they simply “make sense”. Especially in the stock market. All stock markets around the world tend to trend upwards over time. Most major markets steadily climb higher over the decades as more and more wealth is built by nations and corporations (and inflation gradually affects the valuation of hard assets).

This makes trend-following one of the easiest trading styles to stick to through bad times for many traders both retail and professional – assuming you find a trend-following system which performs in a way that suits your personality and financial goals, which I’ll speak about in more detail soon.

It MAKES SENSE that buying the strongest stocks over and over again (and selling them when they no longer become the “strongest” of the bunch) would make you money over time. And ideally, as with Nick’s strategies – much more money than if you were to simply buy and hold stock indexes or ETFs.

Here is an example of Nick’s ASX Momentum Strategy equity curve performance compared to buying and holding the Australian stock market index. This simple trend-following strategy rotates buying the strongest-performing stocks in the Australian stock market at the end of each month (and selling any stocks that are no longer the strongest-performing stocks – which is decided using objective price action indicators):

As you can see, the strategy does have down months and even years sometimes – but overall, this simple trend-following approach works over the long-term to steadily grow and compound returns far in excess of what you would make employing a traditional passive buy & hold strategy.

This makes it “easy” – or at least easier – to stick to a trend-following strategy, at least in theory.

Nothing is easy in trading or investing. But it’s a lot easier to have confidence in what you’re doing if you believe in the underlying theory behind WHY what you’re doing works. Over time stocks tend to trend upwards, and there are always new companies that are growing and expanding their revenue and market valuation.

Unlike some convoluted strategies out there – it doesn’t take a rocket scientist to understand why this approach to investing and trading works.

How to Deal With Drawdowns

As for dealing with drawdowns in an optimal manner – here are a few tips from Nick:

1. Adjust Capital Allocation

If a strategy has a historical drawdown that is higher than what you are comfortable with, you can adjust your risk capital to ensure that if the historical max drawdown occurs again, it will be within your comfortable threshold.

For example, if a strategy has a max historical drawdown of 25% and a trader is only comfortable with a 15% max drawdown, they can divide their preferred max drawdown by the system’s max drawdown to get an allocation modifier:

Adjusted Allocation = Risk Tolerance ÷ Strategy Drawdown

Adjusted Allocation = 0.15 ÷ 0.25

Adjusted Allocation = 0.60 x Capital

In this case, the trader would allocate 60% of their capital to the strategy and then with the remaining capital they could leave it in their bank account accumulating interest (which is not much currently), allocate it to a different strategy, or invest it risk-free with bonds or some such instrument.

One could feasibly also simply trade a position size 40% smaller than the strategy calls for as well, depending on the risk model that is used.

2. Diversify Strategies

Nick is a big fan of diversifying your investments – not by diversifying the markets you trade (although that can obviously be done), but rather through diversifying your strategies.

With his own trading, Nick diversifies the risk of his trend-following systems and offsets their drawdowns by simultaneously employing mean-reversion strategies that operate more short-term.

Having a strategy that trades a different timeframe and/or a different directional bias to your other strategy(s) can reduce the correlated performance of your overall portfolio.

As Nick also points out, since the March 2009 financial crisis Australian shares are up +138% from the lows, whereas American shares in the S&P500 are up a modest +542%. By trading both of these markets with the same strategy you are diversifying your risk across two universes of assets that clearly diverge in correlation at times.

3. Dynamic Position Sizing

Nick points out that famous original Turtle trader Jerry Parker makes a very simple but powerful statement regarding how he deals with drawdowns during an interview:

For every 10% your portfolio declines, decrease your position size by 20%.

This is effectively negative protective compounding – as your account decreases and your drawdown expands, your position size and therefore risk contracts. But as your equity grows and expands, your position sizing increases until you are trading full-size again once the system begins to dig its way out of drawdown.

Click here to read more about what Nick has to say on this subject of methods for dealing with drawdowns.

Nick’s Approach to Trend-Following

Trend-following systems are among the most robust trading styles in existence.

By robust, I mean they are resilient and persistent: they tend to work well across a broad spectrum of markets, and they have worked for a long time – especially in equities.

Recessions and market crashes can of course hurt a trend-following strategy severely, but employing simple filters that revert your portfolio to cash during extended bear markets and recessions can be an effective defense against this risk.

Nick Radge employs these kinds of filters in his stock trading and investing strategies and so far he has avoided catastrophic losses on a yearly return basis.

He calls one such filter an ‘index or regime filter’ – and it simply tells his system to stop trading, enter a protective stance and revert to cash if a key market index falls and stays below a key long-term moving average. Simple, but very, very effective at side-stepping suboptimal trend-following market conditions.

He also tightens his trailing stops when this filter is triggered, ensuring that he doesn’t give too much open profit back to the market if it does turn over into a sustained correction or bear market.

One of the strategies I use to manage part of my own long-term retirement investment portfolio (Nick’s ASX Momentum Strategy) has only had ONE losing year since 2007.

Over the past the past 15 years, Nick’s simple monthly-chart based momentum strategy has returned an average of approximately +20% per year, with a max losing year of -3.70% back in 2018. The max winning year, by comparison, was +59.73% in 2020.

The intra-year drawdowns are much higher than -3.70%, but the end-of-year returns are pretty remarkable given the simplicity of the strategy.

It’s true that, at least in my experience as a trader so far, when it comes to navigating the financial markets using technical analysis – simple is better.

Next I want to explore Nick’s thoughts and approach to system design and how he goes about developing his own trend-following and mean-reversion systems.

Nick’s Philosophy on Trading Systems

Nick has a holistic philosophy surrounding trading systems. The easiest way to portray his thoughts and beliefs around system design is to quote his words directly:

In my definition, a trading system is a broad yet well-defined set of guidelines and instructions, rules and procedures if you like, that quantify the complete trading regime. Now I say the complete trading regime because it has to encompass both the qualitative and quantitative traits of trading itself, the qualitative traits are the emotional side of it all. I can give a person a fabulous trading system, but if they emotionally or psychologically can’t execute that strategy, then regardless of how good it is, you’re not going to be able to use it.

Nick Radge – System Trading

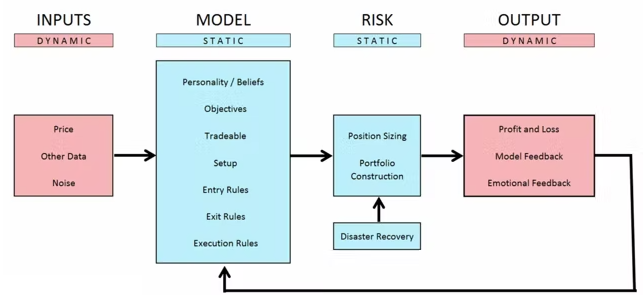

Here is a flow chart diagram Nick uses to explain his fundamental ideas and thesis around system design:

It’s actually quite a simple and logical process that he lays out here.

System Inputs

First, decide on your inputs – for a technical system that will usually be price, but it could also include volume, indicator values, fundamental values (eg. company financials), or even market sentiment or human discretion.

It’s interesting that Nick adds noise as an input as well, implying that he believes noise is inherent in all systems and must be accounted for and expected to influence the system in some way (which is a belief I also share).

He has also highlighted which parts of the system model are dynamic, and which are static.

Obviously a system can be dynamic in all its aspects as the system designer or developer can change anything about the system at any time – but the idea here is that some parts of the system should not be changing once in motion unless absolutely necessary.

The dynamic parts of the system are its inputs and outputs. Price is dynamic and always changing, and so the results or performance of the strategy is always going to be dynamic and changing – but the rules and risk model of the system should not be dynamic and always changing.

The rules and risk model can be adjusted over time if a better method is discovered that has been thoroughly tested and found to improve the results, but this should be a rare occurrence with a robust system.

Once the system is built and tested and found to be profitable within the trader’s psychological and financial risk tolerance (ie. the system makes sense according to their beliefs and personality AND also produces a profit and max drawdown that is within a comfortable range for the trader), then it should be followed rigorously and without hesitation.

System Model

The system model comprises of several important factors that will influence both the strategy’s performance, and the trader’s ability to stick to trading it through bad (and good) times without second-guessing what the system is telling them to do.

This includes the trader’s personality and beliefs about the markets (eg. a trader who is impatient and believes the future is uncertain and thinks markets are completely random and unpredictable may prefer a shorter-term mean-reversion strategy that is quick to get in and quick to get out and perhaps takes both long and short setups, while a patient trader who believes the stock market tends to trend upwards over the long-term may prefer long-only trend-following systems that let trades run for months at a time).

These beliefs can contradict and be incompatible with each other, and yet trading systems can still be built around those core beliefs that produce a profit for both styles of trader. The problem is that even though both traders might build profitable systems, both will be unable to trade each other’s systems and therefore must find their own way that is uniquely suited to them.

The system model also needs to take into account the trader’s objectives. If the trader wants to spend all day sipping margaritas by the pool (which gets boring fast by the way, speaking from experience) then they won’t want to trade a system that requires baby-sitting or requires frequent action from them and may prefer longer-term trend-following systems but with higher risk/reward metrics.

Or if the trader has a day job and a family, they may prefer a strategy that requires less time and input from them but exhibits “safer” risk/reward metrics, and is more conservative. Or the trader might be young and with a high disposable income and plenty of time on their hands and therefore is comfortable trading an active intraday system that has a high average drawdown but high returns.

A system does not necessarily need to be fully automated or even fully systematic with no amount of discretion involved, but it does need to be tradeable, testable and have a confirmed edge over the markets if it is expected to be adhered to.

The point is that a “good” system is different for everyone, and isn’t as simple as one that just makes money.

Although it’s still important that the system does make money, which is where the more practical aspects come into play – such as the markets chosen to be traded, the setup to be traded (ie. your preferred candlestick pattern or market conditions), the entry rules (indicator conditions, filters etc), the exit rules (do you use a trailing stop or do you use a fixed target etc), and your execution rules – for example, do you enter your trades manually or do you automate your system through an API?

All of these aspects combined with your psychological profile interplay to make the perfect system.

Not the perfect system that never loses trades and makes you a millionaire overnight – but the perfect system for you, that you can stick to and have confidence in and execute consistently according to the rules and procedures you lay out for yourself.

System Risk

The next important aspect of system design is your chosen risk model.

This should also be a static aspect of your system design, meaning that once decided upon and tested and found to be acceptable within your system model goals, you should not change this aspect of your system very often – if ever.

There are many different risk models out there to choose from, and there is no such thing as a ‘best’ risk model.

But there are some risk models that are proven and found to improve the performance of most trading strategies and systems, such as equal fixed-fractional dollar models (eg. allocating a fixed 2% of your risk capital per trade regardless of the setup ‘quality’ or stop loss distance) or equal percentage models (eg. a system that trades 10 stocks or assets at a time and allocates 20% of total risk capital to each position).

Here’s another quote directly from Nick reflecting his beliefs around how risk models affect systematic trading strategies:

Risk is actually not a part of the model in my view. It’s an overlay that runs over the top. So position sizing is a core component of that, obviously. Clearly if you have a model with a negative expectancy, doesn’t matter what kind of position sizing you have in place, it’s not going to help you. You need to have a model that’s got a positive expectancy to start with. And from that you can amplify the results using different kinds of position sizing. I don’t think there’s a need to be completely super duper advanced in position sizing. Simple does tend to work reasonably well.

Nick Radge – System Trading

System Output

The final piece of the puzzle when designing trading systems is analyzing feedback. And in financial markets, feedback means P&L – and emotional response.

The more obvious output is your risk-adjusted returns, but a lesser addressed output is how your strategy makes you feel. If your strategy makes you feel too anxious or uncomfortable, then you won’t be able to stick to it.

Now, all strategies will make you anxious or uncomfortable at some point – or else you wouldn’t be a trader. But you need to ensure your system performs within a comfortable emotional range as well as within a comfortable risk/return range.

If you can’t handle large or long-enduring drawdowns and your system is profitable, but regularly encounters months of no new equity highs or sharp and scary drawdowns, you won’t be able to stick to it even if it would still make you money in the long-term. This is an important consideration to make when building your own systems and strategies.

A system might look fantastic on paper and make tons of money, but when you start trading it in realtime, it makes you too uncomfortable to keep pulling the trigger. In such a case you would be better off trading a different strategy that perhaps returns less money, but also experiences less exposure risk.

Now in terms of P&L – all trading systems depend on being ‘in sync’ with the market at times in order to make money, according to Nick’s philosophy, if you can call it that. It’s not really a philosophy so much as an objective observation of reality.

A trading system cannot be perfect; it will have losing trades, because the future is unpredictable and no model, no matter how sophisticated or accurate, can 100% accurately predict the future. If you find one, please let me know – I’ll send you all of my money.

This by definition means that a strategy will have ‘better days’ and ‘worse days’ over the long-term. The better days or profitable periods will occur when the system is ‘in sync’ with the market. For a trend-following approach as an example, this would mean the market is trending.

If the market is going sideways, it is going to be ‘out of sync’ with a trend-following model, and therefore trend-following models are extremely likely to experience a (very natural and expected) drawdown.

And by implication, a mean-reversion or counter-trend model during this time is likely to be ‘in sync’ with the market and will probably be making money while these other models that depend on momentum or trending conditions are losing money, and that’s why Nick encourages the diversification of strategies as a systems trader.

Another quote from Nick:

Because a market and price action is dynamic and your model is static, then you will always at some stage be out of sync with the market. It is absolutely impossible to build a robust strategy, which we’ll talk about shortly, that looks to profit in every kind of market environment. That doesn’t exist, at least not in any robust format that I’ve ever come across and many professional traders who manage hundreds of millions of dollars.

Nick Radge – System Trading

Basically, Nick is saying that drawdowns are inevitable no matter how robust or effective your strategy is at capitalizing on various market conditions or forms of behavior.

However over time you will get enough feedback from the market in the form of performance metrics that will help guide you in improving the system over time, and this valuable feedback can be used to then tweak the inputs of the system (or the risk model), in turn influencing the feedback in a (hopefully) positive manner, and the cycle continues indefinitely.

There is a risk of over-optimizing strategies based on the output and feedback of the strategy which traders must be wary of – the goal with using system feedback to adjust input parameters and aspects of the system to improve it should not be mistaken for curve-fitting the strategy.

Curve-fitting is when a trader adjusts elements of the strategy to improve its performance purely on historical data, without necessarily improving the robustness or the future performance of the system on realtime data, which is always changing, adapting, and playing out slightly different to the past (or sometimes radically differently).

A robust strategy, or a strategy that is resilient and likely to stand the test of time well into the future, should be one that performs well-enough on historical data without being overly optimized to a market’s past behavior. And in fact, a truly robust strategy will work well not just on the historical data of one market – but many markets, at least a handful, and ideally many different timeframes too.

There are many ways to measure the robustness of a strategy which we won’t get into in today’s article as it deserves its own post altogether, but one consideration is Monte Carlo simulations – or randomly adjusting samples in your testing data to introduce a degree of randomness over several simulations.

If your strategy is profitable over dozens or hundreds of semi-randomized simulations, and especially over multiple markets and/or timeframes, then you probably have a fairly robust strategy that will continue to have an edge well into the future.

In my early days as a trader I definitely fell into the trap of curve-fitting strategies based on recent price data.

I’ve traded several intraday strategies over the past few years that I built to perform well on the forex markets, but the strategy did not hold up on price data past a few years – meaning the strategy I was trading was suited to taking advantage of how price had behaved over the past year or two, but was not robust and did not perform well over many markets or timeframes.

It has been my experience that these strategies do work for a time, but not as well as you’d expect based on their historical performance on the market and timeframe it was optimized for, and in some cases the ‘edge’ of the strategy can fade rapidly as markets evolve and conditions change.

This is a difficult tight rope to navigate as optimization of a system can lead to increasing its robustness if done correctly, but it can also lead to curve-fitted strategies if taken to the extreme or done incorrectly which can actually reduce the robustness of a strategy.

This is a complex subject that perhaps deserves its own article (especially as I learn more about it myself), so I’ll leave these thoughts here and move on for now.

Conclusion / Learn More

I recently purchased a systematic trading development mentorship program from Nick Radge worth $15,000 – the most amount of money I’ve spent on my trading education so far – and it has been worth every penny.

I’m learning a LOT about robust systematic equity strategy development and testing, including fully-automated trading systems. I’ll be covering some of the things I learn and the experiences I have on my blog and YouTube channel over the months and years to come.

I’m a huge fan and advocate of Nick’s trading style, his transparency and honesty, and his experience as a veteran trader who has been through every market condition from euphoria to terror over the past few decades.

I highly encourage any traders who like my work and reflections to check out his work, too, as we share many same core beliefs about trading and financial markets (except that he’s much better looking and experienced than I am).

Note: Nick Radge runs a signal service through his company TheChartist where you can follow the exact trades he takes with several of his trading systems. I personally use this service to manage a portion of my capital – if this sounds interesting to you click here to get 10% off your annual subscription (includes 2-week free trial).

If you want to learn more about Nick’s trading style and hear about his experiences in the markets, check out his website, these two brilliant podcast episodes done by Aaron Fifield of ChatWithTraders, and a short video interview:

What a quality article – well done.